![]()

AUGUST • VOL. 6 • SERIES OF 2024

INSIGHTS is a monthly publication of BDB LAW to inform, update and provide perspectives to our clients and readers on significant tax-related court decisions and regulatory issuances (includes BIR, SEC, BSP, and various government agencies).

DISCLAIMER: The contents of this Insights are summaries of selected issuances from various government agencies, Court decisions, and articles written by our experts. They are intended for guidance only and as such should not be regarded as a substitute for professional advice.

Copyright © 2024 by Du-Baladad and Associates (BDB Law). All rights reserved. No part of this issue covered by this copyright may be produced and/or used in any form or by any means – graphic, electronic, and mechanical without the written permission of the publisher.

What's Inside ...

- HIGHLIGHTS FOR JULY 2024

- SIGNIFICANT COURT DECISIONS

- Court of Tax Appeals

- SIGNIFICANT REGULATORY ISSUANCES

- Bureau of Internal Revenue

- Securities and Exchange Commission

- PUBLISHED ARTICLE

- Creditable Withholding Tax (CWT) Refund Claims

- OUR EXPERTS

- The Personalities

- The Personalities

HIGHLIGHTS for JULY 2024

COURT OF TAX APPEALS DECISIONS

- For products to be classified as milk products and be excepted from sweetened beverage tax: (i) it must be determined by the FDA to fall under the milk product category; and (ii) it must not be excluded from this category. (Nestle Philippines, Inc. v. Commissioner of Internal Revenue, CTA EB NO. 2711 (CTA Case No. 9943), July 11, 2024)

-

Non-submission of the documents for refund would not ipso facto result in the denial of the claim for tax refund or credit. (Ford Group Philippines, Inc. vs. Commissioner of Internal Revenue, CTA Case No. 10507, July 10, 2024)

-

The vital element in determining the validity of the assessment is the definiteness of the amount indicated in the FLD and the deadline for payment. (Li-Son Transport Service Inc. v. Commissioner of Internal Revenue, C.T.A. Case No. 10631, July 23, 2024)

-

The Court ruled that the proper remedy for the taxpayer was to file a Petition for Review before the CTA within 30 days from receipt of the FDDA. (Pentagon Gas Corporation v. Commissioner of Internal Revenue and Manuel V. Mapoy, in his capacity as OIC-Asst Commissioner, Large Taxpayers Service, CTA Case No. 10868, July 19, 2024)

- A Letter Notice must first be converted to an LOA before a revenue officer may proceed with the further examination and assessment of a taxpayer. (Republic of the Philippines v. Mr. Ranson Diodell N. Tenerife doing business under the name “MOTORINA TRADING”, CTA EB No. 2805 (CTA OC No. 025), July 10, 2024)

- Beginning June 1, 2010, the revalidation of a LOA if the audit is not completed within 120 days is no longer a requirement. (Strawberry Foods Corporation, v Commissioner of Internal Revenue, CTA Case No. 10282, July 12, 2024)

- One of the basic requirements for entitlement to claim for refund or issuance of tax credit certificate is that a taxpayer is the statutory taxpayer and it actually paid the claimed excise taxes on the same petroleum products sold to the tax-exempt entity. (SL Harbor Bulk Terminal Corporation. v. Commissioner of Internal Revenue, CTA Case No. 10250, July 26, 2024)

BIR ISSUANCES

- Revenue Memorandum Order, July 03, 2024 – This provides for the Guidelines, Policies and Procedures in the Processing of Claims for Tax Credit/Refund of Excess/Unutilized Creditable Withholding Taxes On Income.

- Revenue Memorandum Order, July 03, 2024 – This provides for the Guidelines, Policies and Procedures in the Processing of Claims for Credit/Refund of Taxes Erroneously or Illegally Received or Collected or Penalties Imposed Without Authority.

- Revenue Memorandum Circular No. 75-2024, July 3, 2024 - This prescribes the mandatory requirements for claims for tax credit or refund of excess/unutilized CWT on income pursuant to Section 76(C), in relation to Section 204(C) and 229, of the NIRC, as amended, except those under the authority and jurisdiction of the Legal Group.

- Revenue Memorandum Circular No. 74-2024, July 3, 2024 - This prescribes the mandatory requirements for claims for credit/refund of taxes erroneously or illegally received or collected or penalties imposed without authority pursuant to Section 204(C), in relation to Section 229, of the NIRC, as amended, except those under the authority and jurisdiction of the Legal Group.

- Revenue Memorandum Circular No. 77-2024, July 11, 2024 - This provides for the clarification on the invoicing requirements provided under RR No. 7-2024, as amended by RR No. 11-2024.

- Revenue Memorandum Circular No. 79-2024, July 15, 2024 - This further extends the transitory period prior to actual imposition of withholding tax on gross remittances made by digital financial services providers to sellers/merchants prescribed under RR No. 16-2023.

SEC ISSUANCES

- SEC Memorandum Circular No. 10, July 10, 2024 – Prescribes new guidelines for Electronic SEC Universal Registration Environment (ESECURE).

- SEC Memorandum Circular No. 11, July 11, 2024 – The SEC mandates all publicly listed companies to upload the minutes of the regular and special stockholders’ meetings.

- SEC Memorandum Circular No. 12, July 16, 2024 – Prescribing new guidelines in Securing and Expanding Capital in Real Estate Investments Transactions.

SEC OPINION

- SEC OGC Opinion No. 24-14, dated May 21, 2024, posted July 26, 2024 – The right of a stockholder to inspect corporate records is not absolute and is subject to certain limitations and penalties.

- SEC OGC Opinion No. 24-16, dated June 18, 2024, posted July 26, 2024 – A foreign national can be legally elected as a director of the Corporation that is not a public utility.

- SEC OGC Opinion No. 24-19, July 26, 2024 – A Domestic Market Enterprise is an enterprise that produces goods for sale, or renders services to the domestic market entirely or not exporting sixty (60) percent or more of its output.

- SEC OGC Opinion No. 24-20, July 26, 2024 – The Corporation does not have to register with the Commission as a financing company considering its activities are not those of a financing company.

- SEC OGC Opinion No. 24-17, dated June 19, 2024, posted July 26, 2024 – The Corporation does not have to register with the Commission as a financing company considering its activities are not those of a financing company.

Non-submission of the documents for refund would not ipso facto result in the denial of the claim for tax refund or credit.

The taxpayer filed its Annual ITR and Amended Annual ITR for CY 2018. However, due to inaction, it elevated its claim for refund to the CTA. The taxpayer argued that the claim for refund should be granted because all necessary elements are present to grant the claim. On the other hand, the BIR contends that failure on the part of the taxpayer to submit relevant documents on the administrative level makes the administrative claim for refund or credit pro forma and shall be construed as if no administrative claim was filed at all.

The Court ruled that a review of RMO No. 53-98 and RR No. 2-2006 does not indicate that the non-submission of the enumerated documents would ipso facto result in the denial of the claim for tax refund or credit. RR No. 2-2006 merely imposes a penalty of fine for non-submission of the information or statement required therein, but not the outright denial of any tax refund or credit claim.

The Court further ruled that, even if the taxpayer failed to submit the complete documents at the administrative level, it would not render its Petition for Review dismissible. The Court may give credence to all evidence presented by the taxpayer including those that may not have been submitted at the administrative level. (Ford Group Philippines, Inc. vs. Commissioner of Internal Revenue, CTA Case No. 10507, July 10, 2024)

The vital element in determining the validity of the assessment is the definiteness of the amount indicated in the FLD and the deadline for payment.

The taxpayer received the FLD/FAN which demanded payment of the same basic tax deficiencies as stated in the PAN. The taxpayer sent a letter to the BIR, denominated as a "Request for Reinvestigation." Subsequently, the BIR served the WDL.

The taxpayer then filed a Petition for Review and contends that the FLD/FAN is void for failing to (a) demand the payment of tax liabilities; (b) indicate the due date for payment; and (c) fix the amount of interest due.

The Court ruled that the vital element in determining the validity of the assessment is the definiteness of the amount indicated in the FLD and the deadline for payment (shown in the assessment notices attached to the FLD). If the FLD substantially satisfies both requirements, then the FLD could not be said to be wanting of material details nor should the assessment be voided based on such premise.

Here, the mere use of the phrase "you are requested to pay your aforesaid deficiency..." cannot invalidate the said FLD/FAN. In fact, the same phraseology is used in the pro-forma Formal Letter of Demand in Annex B of RR No. 12-99, as amended by RR No. 18-2013. As to the due date, the FLD clearly identifies the due date of the assessment. (Li-Son Transport Service Inc. v. Commissioner of Internal Revenue, C.T.A. Case No. 10631, July 23, 2024)

The Court ruled that the proper remedy for the taxpayer was to file a Petition for Review before the CTA within 30 days from receipt of the FDDA.

The taxpayer was assessed for deficiency IT, VAT, EWT, DST, and compromise penalties. The taxpayer received the FDDA in June 2021. Instead of appealing to this Court, the taxpayer opted to file a letter-reply to the FDDA before the office of the CIR. On March 2022, the taxpayer issued a WDL to collect the alleged IT and VAT liabilities. Aggrieved with the issuance of the WDL, on 24 March 2022, the taxpayer transmitted its letter, reiterating its previous request for reconsideration and re-computation of the deficiency assessments. Disregarding the taxpayer's pleas, the BIR issued WG which was received by the taxpayer on 02 May 2022. On 27 May 2022, the taxpayer filed before this Court a Petition for Review. The BIR contended that the taxpayer failed to file the Petition despite its receipt of the FDDA. Due to its failure to contest the FDDA, they accordingly became final and executory.

The Court ruled that the proper remedy for the taxpayer was to file a Petition for Review before the CTA within 30 days from receipt of the FDDA. As provided clearly in Section 3.1.4 of RR No. 12-99, as amended by RR No. 18-13, the taxpayer’s resort to file an MR with the CIR did not toll the running of the 30-day prescriptive period to appeal before the CTA.

Here, almost two (2) years have lapsed from the taxpayer's receipt of the CIR's final decision (or the FDDA) before it filed an appeal with this Court. Considering the amount of time that elapsed, this Court's lack of jurisdiction to entertain the original Petition for Review becomes indisputable. (Pentagon Gas Corporation v. Commissioner of Internal Revenue and Manuel V. Mapoy, i his capacity as OIC-Asst Commissioner, Large Taxpayers Service, CTA Case No. 10868, July 19, 2024)

A Letter Notice must first be converted to an LOA before a revenue officer may proceed with the further examination and assessment of a taxpayer.

The taxpayer received the BIR’s Letter Notice (“LN”), informing him that he has undeclared local purchases. Subsequently, the BIR issued an FLD and FAN, with details of discrepancies assessing the taxpayer.

The CTA in Division ruled that the FLD and FAN with Details of Discrepancies issued by the BIR against the taxpayer is void because the audit or examination conducted by the BIR personnel has no prior permission from the CIR or his duly authorized representatives. The BIR argues that a LN also serves as a LOA.

The CTA En Banc ruled that an LN must first be converted to an LOA before a revenue officer may proceed with the further examination and assessment of a taxpayer. An examination and assessment of a taxpayer without prior issuance of an LOA is tantamount to a violation of due process rendering the assessment void. (Republic of the Philippines v. Mr. Ranson Diodell N. Tenerife doing business under the name “MOTORINA TRADING”, CTA EB No. 2805 (CTA OC No. 025), July 10, 2024)

For products to be classified as milk products and be excepted from sweetened beverage tax: (i) it must be determined by the FDA to fall under the milk product category; and (ii) it must not be excluded from this category

This is an appeal on the Decision of the CTA – Third Division denying the refund claim of the taxpayer on its erroneously paid Sweetened Beverage Taxes (SBT) on its product MILO®, a powdered chocolate malt-flavored milk drink.

The taxpayer submits that its MILO® products are not subject to SBT as they are properly classified as "flavored milk" based on the Food Category Descriptors of the Codex Alimentarius Food Category Descriptors (CODEX), thereby, excluded from the imposition of SBT.

The Court ruled that taxpayer’s MILO products must satisfy two criteria to be classified a milk product per CODEX: (i) they must be determined by the FDA to fall under this milk product category; (ii) they must not be excluded from this category.

As to the first criterion, the taxpayer’s MILO products apparently fall under “flavored fluid milk drinks” considering that the product names thereof commonly include "MILK DRINK" and they belong to the food categorization "HRA 1b. Dairy-based drinks, flavored and/or fermented", as indicated in the FDA-issued Certificates of Product Registration and the Application Details. Moreover, based on the description of the term "flavored fluid milk drinks," the examples enumerated under the description of the said term specifically include “chocolate malt drinks.”

As to the second criterion, taxpayer’s MILO® products cannot be classified as "mixes for cocoa (cocoa-sugar mixtures)". This is because such a sub-food category is supposed to contain only cocoa powder and sugar. Also, "finished cocoa beverages and chocolate milk" are explicitly included in Food Category for "flavored fluid milk drinks", and therefore, they are necessarily excluded from the Food Category for cocoa-sugar mixtures.

The Court finds that the taxpayer’s MILO® products as not subject to SBT for being classified as a 'milk product' under the sub-food category "flavored fluid milk drinks". Consequently, the taxpayer is entitled to the refund of the excise taxes it paid. (Nestle Philippines, Inc. v. Commissioner of Internal Revenue, CTA EB NO. 2711 (CTA Case No. 9943), July 11, 2024)

Beginning June 1, 2010, the revalidation of a LOA if the audit is not completed within 120 days is no longer a requirement.

This is an appeal on the assessment issued by the BIR against the taxpayer covering TY2014. Taxpayer argues that the examination conducted is illegal because the handling RO continued with the audit and examination despite the lapse of the 120-day period, sans revalidation of such LOA. Conversely, the BIR counters that the revalidation requirement invoked by taxpayer is no longer controlling, in view of RMO No. 44-2010.

The Court held that beginning June 1, 2010, RMO No. 44-2010 brushed aside the revalidation requirement, if the assigned RO failed to complete the audit, within one hundred twenty (120) days from issuance of the LOA.

In this case, since the period covered by LOA is from January 1, 2014, to December 31, 2014, the failure of RO Tamayo to complete the audit within such 120-day period, sans revalidation of such LOA, does not result in the nullification of said BIR audit or examination for TY 2014. The audit/examination conducted by the BIR in this case is for TY 2014 which was after the issuance of RMO No. 44-2010. (Strawberry Foods Corporation, v Commissioner of Internal Revenue, CTA Case No. 10282, July 12, 2024)

One of the basic requirements for entitlement to claim for refund or issuance of tax credit certificate is that a taxpayer is the statutory taxpayer and it actually paid the claimed excise taxes on the same petroleum products sold to the tax-exempt entity.

The taxpayer filed an administrative claim for tax credit with the BIR covering excise taxes paid. The taxpayer argues that it is entitled to a tax credit for the erroneously paid excise tax on the bunker fuel and diesel which it imported and allegedly have been used to sell Bunker Fuel Oil and Special Fuel Oil to entities registered with Subic Bay Metropolitan Authority (SBMA) and Philippine Economic Zone Authority (PEZA). On the other hand, BIR counters that taxpayer is not entitled to its claim for refund.

The Court ruled that one of the basic requirements for entitlement to claim for refund or issuance of tax credit certificate is that a taxpayer is the statutory taxpayer and it actually paid the claimed excise taxes on the same petroleum products sold to the tax-exempt entity.

In this case, while the Court found that the taxpayer is the statutory taxpayer and that the excise taxes were paid based on supporting documents, particularly, the Statement of Settlement of Duties and Taxes. However, despite this, the taxpayer failed to trace the fuel movements showing that the subject sales came from the importations with excise tax paid. (SL Harbor Bulk Terminal Corporation. v. Commissioner of Internal Revenue, CTA Case No. 10250, July 26, 2024)

Revenue Memorandum Order No. 25-2024 July 3, 2024 - This provides for the guidelines, policies, and procedures in the processing of claims for tax credit/refund of excess/unutilized Creditable Withholding Taxes (CWT) on income.

The following are to be observed in the processing of claims for tax credit/refund of excess unutilized CWT:

- The processing offices authorized to receive the application are as follows:

- Revenue District Office (RDO)

- Large Taxpayers Audit Division (LTAD) or Large Taxpayers District Office (LTDO) under the Large Taxpayers Service (LTS)

- Only applications with complete documentary requirements enumerated in the attached Checklist of Mandatory Requirements shall be received and processed.

- For regular applications or those filed by taxpayers of “going-concern” status:

- Filing of the application shall be made within two (2) years from date of filing of the AITR. A return filed showing an overpayment shall be considered as a written claim for tax credit/refund. Submission of complete documents shall commence the counting of the 180-day processing period.

- Income upon which taxes are withheld must be included as part of gross income declared in the AITR.

- Fact of withholding is established by a copy of the withholding tax certificate.

-

Strict observance to the 180-day time frame to grant in full or in part the claims for tax credit/refund of CWT.

-

The result of the verification of the claim, whether approval or denial, shall be communicated to the taxpayer-claimant.

- Should the taxpayer-claimant opt to elevate the full or partial denial of the claim of the Court of Tax Appeals (CTA):

- In case of full or partial denial, the taxpayer may, within thirty (30) days from the receipt thereof, appeal the decision with the CTA.

- In case the tax credit/refund is not acted upon within the 180-day period, the taxpayer may opt to appeal to the CTA within the 30-day period

- After the expiration of the 180 days required by law to process the claim, the taxpayer may opt to forego the judicial remedy and await the final decision.

- When no decision is rendered within the 180-day period and the taxpayer opted to seek for a judicial remedy within 30 days from such period, the administrative claim for refund shall be considered moot and shall no longer be processed.

- The claims for erroneously or illegally collected tax credit/refund must conform with the following essential requisites:

- The tax credit/refund claim pertains to erroneously or illegally received or collected taxes or penalties imposed without authority.

- Filing of a claim for tax credit/refund shall be done within two (2) years after payment of the tax or penalty.

- The erroneously or illegally received or collected taxes must be supported with a copy of the duly filed tax return with the corresponding payment remitted to the Bureau.

- The processing offices authorized to receive the application are the following:

- The Revenue District Office (RDO); or

- The respective Large Taxpayers Audit Division (LTAD) or Large Taxpayers District Office (LTDO) under the Large Taxpayers Service (LTS).

- The following offices shall be responsible in the processing, review, and approval of claims regardless of the amount:

| Processing Office | Reviewwing Office | Approving Official |

| RDO | Assessment Division | Regional Director |

| LTAD/LTDO | Head Revenue Executive Assistant, LTS | Assistant Commissioner, LTS |

-

The time frame to grant in full or in part the claims is 180 days from the date of submission of complete documents in support of the application.

-

Only applications with complete documentary requirements shall be received and processed by the authorized processing office.

-

The result of the verification of the claim, whether approval or denial, shall be communicated to the taxpayer-claimant, which shall be signed by the authorized revenue official and shall be served by the originating processing office.

-

The following rules shall govern should the taxpayer-claimant opt to elevate the full or partial denial of the claim of the Court of Tax Appeals (CTA):

- In case of full or partial denial of the claim, the taxpayer affected may, within thirty (30) days from the receipt, appeal the decision with the CTA.

- In case the tax credit/refund is not acted upon within the 180-day period, the taxpayer may opt to appeal to the CTA within the 30-day period after the expiration of the 180 days to process the claim.

- The taxpayer may also opt or forego the judicial remedy and await the final decision.

- When no decision is rendered within the 180-day period and the taxpayer- claimant opted to seek for a judicial remedy within 30 days from such period, the administrative claim for refund shall be considered moot and shall no longer be processed.

Revenue Memorandum Circular No. 75-2024, July 3, 2024 – This prescribes the mandatory requirements for claims for tax credit or refund of excess/unutilized CWT on income, except those under the authority and jurisdiction of the Legal Group.

- Three (3) original copies of duly accomplished Application for Tax Credit/Refund (BIR Form No. 1914);

- Application for Registration Information Update/Correction/Cancellation (BIR Form No. 1905) [For taxpayers that have ceased or dissolved business];

- Authenticated copy of the Board Resolution (for Partnership/Corporation) for the shortening of the Corporate Term [For taxpayers that have ceased or dissolved business];

- AFS complete with Notes to AFS, if AFS was not submitted in the BIR eAFS Facility;

- Original copies of duly accomplished Certificate of Creditable Tax Withheld at Source (BIR Form No. 2307) or Withholding Tax Remittance Return for Onerous Transfer of Real Property Other Than Capital Asset (BIR Form No. 1606), whichever is applicable, issued by the payor (withholding agent) to the payee;

- Hard and soft copies (in MS Excel format) of Summary Revenues/Income declared per Income Tax Return (ITR) and the corresponding taxes withheld per BIR Form No. 2307/1606 in accordance with the format prescribed;

- Original copy of the duly notarized Taxpayer’s Attestations;

- Original copy of Notarized Secretary’s Certificate (for corporate claimant) or SPA (for individual & ROHQ claimant) stating the authorized representative/s to file, sign documents on behalf of the claimant and/or follow-up tax credit/refund claims together with the photocopy of at least one (1) valid government-issued ID with three (3) specimen signatures of authorized representative/s; and

- Original copy of Delinquency Verification Certificate (valid for 6 months) issued by the Collection Division under the respective

- Revenue Region or the LT-Collection Enforcement Division under the Large Taxpayers Service, whichever is applicable.

The foregoing shall be submitted to the processing office that has jurisdiction over the taxpayer-claimant as follows:

- The RDO; or

- The respective Large Taxpayers Audit Division (LTAD) or Large Taxpayers District Office (LTDO) under the Large Taxpayers Service (LTS).

RMC No. 74-2024, July 3, 2024 – This prescribes the mandatory requirements for claims for credit/refund of taxes erroneously or illegally received or collected or penalties imposed without authority, except those under the authority and jurisdiction of the Legal Group.

The claim for credit/refund must be accompanied with the following supporting documents:

- Three (3) original copies of duly accomplished Application for Tax Credit/Refund (BIR Form No. 1914);

- Letter addressed to the CIR stating therein the legal basis, facts, and other circumstances justifying the claim for tax credit/refund;

- Copy of the duly filed tax return with the corresponding proof of payment remitted to the BIR;

- Original copy of the duly notarized Taxpayer’s Attestations;

- Original copy of Notarized Secretary’s Certificate (for corporate claimant) or SPA (for individual & ROHQ claimant) stating the authorized representative/s to file, and sign documents on behalf of the claimant and/or follow-up tax credit/refund claims together with the photocopy of at least one (1) valid government-issued ID with three (3) specimen signatures of authorized representative/s;

- Original copy of Delinquency Verification Certificate (valid for 6 months) issued by the Collection Division under the respective Revenue Region or the LT-Collection Enforcement Division under the Large Taxpayers Service, whichever is applicable; and

- Other documentary requirement(s) in support of the claim.

The foregoing shall be submitted to the processing office that has jurisdiction over the taxpayer-claimant as follows:

- The RDO; or

- The respective Large Taxpayers Audit Division (LTAD) or Large Taxpayers District Office (LTDO) under the Large Taxpayers Service (LTS).

The taxpayer-claimant must file the application with complete documentary requirements within the prescribed two-(2-) year period after the payment of the tax or penalty.

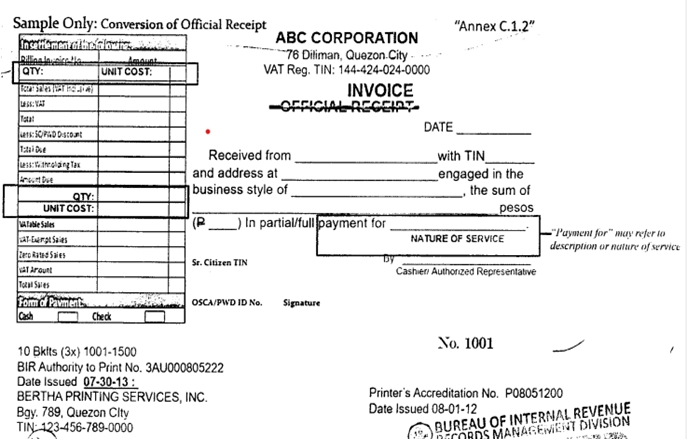

Revenue Memorandum Circular No. 77-2024, July 11, 2024 – This provides for the clarification on the invoicing requirements provided under RR No. 7-2024, as amended by RR No. 11-2024.

Taxpayer has the option to use the remaining unused booklets of ORs as follows:

- As a supplementary document

1. Each page of the unused OR must be stamped with the phrase “THIS DOCUMENT IS NOT VALID FOR CLAIM OF INPUT TAX.”

2. Failure to do so will not make the document a valid replacement for the invoice.

- Convert and use the remaining ORs as invoice until they are fully consumed

1. The word “Official Receipt/Billing Statement/Statement of Account/Statement of Charges into Billing Invoice” on the face of the manual and loose leaf printed receipt shall be stricken out [e.g. Official Receipt] and be stamped “Invoice” or “Cash Invoice” or “Charge Invoice” or “Credit Invoice” or “Service Invoice” or [e.g. Billing Statement] “Billing Invoice”, or any name describing the transaction for which such invoice shall be issued to its buyer/purchaser.

2. The converted Invoice/Billing Invoice shall contain the required information provided under RR No. 7-2024, as amended, including details like quantity, unit cost, and description or nature of service pursuant to Sec. 237 of the Tax Code.

3. Missing information may be stamped on the document if not originally included, upon conversion.

4. Shall apply for a new ATP.

Taxpayer has the option to use the remaining unused booklets of ORs

Sample conversion of OR to Invoice:

Revenue Memorandum Circular No. 79-2024, July 15, 2024 - This further extends the transitory period prior to actual imposition of withholding tax on gross remittances made by digital financial services providers to sellers/merchants prescribed under RR No. 16-2023.

In order to provide additional time to the digital financial services providers, the prescribed transitory period is further extended for another ninety (90) days or until October 12, 2024.

Meanwhile, all electronic marketplace operators shall impose the withholding of tax to sellers/merchants beginning July 15, 2024.

SEC Memorandum Circular No. 10, July 10, 2024

Prescribes new guidelines for Electronic SEC Universal Registration Environment (ESECURE).

The Commission creates the eSECURE, an online platform that grants simplified access to the following online services:

- eSPARC

- OneSEC

- ACES

- eSEARCH

- SEC API Marketplace

- eRAMP

- eFAST and SEC EASE

- eAMEND

- SEC Appointment System

- SEC iMessage

To secure an eSECURE account, the individual shall upload a copy of the PhilSys ID or any 2 government-issued IDs. Anyone with a credentialed eSECURE may digitally authenticate documents that will be submitted to the Commission.

Subject to existing laws, the Commission shall accept the submission of electronic documents without the required notarization, apostille, or authentication when the documents are authenticated by users of eSECURE. (SEC Memorandum Circular No. 10, July 10, 2024)

SEC Memorandum Circular No. 11, July 11, 2024 - The SEC mandates all publicly listed companies to upload the minutes of the regular and special stockholders’ meetings.

The minutes of the meeting shall include the following:

A. Date, time, and place of the meeting

B. List of attendees

C. Determination of quorum

D. Agenda discussed and resolutions reached

E. Description of the voting and vote tabulation

F. Record of the voting results for each agenda

G. That the stockholders were given the opportunity to ask questions

H. Record of the questions asked and answers given.

The minutes shall be posted on the Company website within 5 business days from the date of the meeting. Penalties shall be imposed for non-compliance. (SEC Memorandum Circular No. 11, July 11, 2024)

SEC Memorandum Circular No. 12,

July 16, 2024 - Prescribing new guidelines in Securing and Expanding Capital in Real Estate Investments Transactions (SEC RENT).

The SEC now requires clearance and registration before issuance of securities by real estate brokers in relation to rental pool agreements.

After securing clearance from the Markets and Securities Regulation Department, the Company Registration and Monitoring Department, the Corporate Governance and Finance Department, the Enforcement and Investors Protection Department, and the Office of the General Accountant, the registrant must perform the following actions:

A. Present its financial statements to the Office of the General Accountant for pre-evaluation.

B. Email digital copies of the following documents to msrd@This email address is being protected from spambots. You need JavaScript enabled to view it. in both Word and PDF format:

- OGA Pre-Evaluation Clearance Form;

- SEC Rent Pre-evaluation Checklist Form

- Form SEC RENT and Prospectus; and

- All required Exhibits

C. Submit 2 sets of hard copies of the documents and pay the assessed registration

The registrant must upload all its required reports in the official website. Upon approval, the MSRD shall issue an Order of Registration and/or Permit to Sell Securities to the Public.

The registrant shall submit digital copies of monthly reports on the number of shares sold and other reports required by relevant rules and regulations. (SEC Memorandum Circular No. 12, July 16, 2024)

SEC OGC Opinion No. 24-14, dated May 21, 2024, posted July 26, 2024 - The right of a stockholder to inspect corporate records is not absolute and is subject to certain limitations and penalties.

The Corporation seeks answers to its question of whether their stockholder is entitled to the right to inspect certain voluminous and extensive corporate records. While the SEC did not provide a categorical opinion, they provided the following information.

While the general rule is to recognize and uphold the exercise of the right to inspect the affairs and finances of the corporation, such rule is limited by provisions of the Revised Corporation Code. However, the burden to prove propriety of the examination rests on the Corporation.

The stockholders who abuse their right to inspect corporate documents shall be subject to certain penalties under the Intellectual Property Code of the Philippines, the Data Privacy Act, and the Revised Corporation Code. The stockholders who do procure information are also bound by confidentiality rules under prevailing laws. (SEC OGC Opinion No. 24-14, July 16, 2024)

SEC OGC Opinion No. 24-16, dated June 18, 2024, posted July 26, 2024 - A foreign national can be legally elected as a director of the Corporation that is not a public utility.

The Corporation seeks to answer the question of whether a foreigner can be legally elected as their director, on the ground that the Corporation was no longer a public utility under the amended PSA.

Based on the amended PSA, the limitations on foreign ownership do not apply to those performing public services not included in a selective list, such as corporations engaged in the airline business. Thus, foreign equity restrictions no longer apply to the Corporation. As a result, provided that the foreigner possesses all of the qualifications and none of the disqualifications provided by the Revised Corporation Code, the foreign national can be legally elected as a director of the Corporation. (SEC OGC Opinion No. 24-16, July 16, 2024)

SEC OGC Opinion No. 24-19, July 02, 2024 - A Domestic Market Enterprise is an enterprise that produces goods for sale, or renders services to the domestic market entirely or not exporting sixty (60) percent or more of its output.

The Corporation inquired whether they are engaged in a wholly or partially nationalized business activity under the Anti-Dummy Law. The Corporation is a wholly-owned subsidiary of a subsidiary of a domestic corporation engaged in IT solutions.

A Domestic Market Enterprise is an enterprise that produces goods for sale, or renders services to the Domestic Market not exporting 60% or more of its product. However, the SEC ruled that there was a lack of information on whether the Corporation serves the domestic market entirely or does not export 60% or more of its output. Given that the Corporation would not fall anywhere else, the SEC could not reasonably determine whether the Corporation is engaged in a wholly or partially nationalized business activity. (SEC OGC Opinion No. 24-19, July 16, 2024)

SEC OGC Opinion No. 24-20, July 16, 2024 - The Corporation does not have to register with the Commission as a financing company considering its activities are not those of a financing company.

The Corporation seeks clarification on the exact nature of their transactions and whether they will need registration under the Financing Company Act.

The Corporation does not have to register with the Commission as a financing company since its activities are not those of a financing company. Nonetheless, it is still required to register as an ordinary domestic corporation.

In testing whether the Corporation was engaged in financing company activities, the SEC held that the Corporation was not extending credit, and it was only acting as an agent of the financing companies. (SEC OGC Opinion No. 24-20, July 16, 2024)

SEC OGC Opinion No. 24-17, dated June 19, 2024, posted July 26, 2024 -

Retail Trade cannot be expansively construed to also include online stores within the ambit of a “single outlet”.

The Corporation inquired about their sales conducted through online selling meet the criteria for classification as single outlet sales, thereby qualifying them for exemption under the Retail Trade Liberalization Act.

The SEC referred to a previous opinion that Retail Trade cannot be expansively construed to also include online stores within the ambit of a “single outlet”. The definition of retail trade does not distinguish between retail trade through physical stores and through online channels. At most, selling online is just a new mode of delivering retail services. (SEC OGC Opinion No. 24-17, July 16, 2024)

Creditable Withholding Tax (CWT) Refund Claims

By Atty. Mabel L. Buted

Early this year, when the Ease of Paying Taxes Act (EOPT) was passed into law, I wrote about the reforms and changes introduced by the said law in relation to the processing of claims for refund of excess and unutilized creditable withholding taxes (“CWT”) of taxpayers. It can be recalled that the EOPT has already set a definite period within which our tax authority should act upon these claims for refund. The BIR is granted a period of 180 days from submission of complete documents to decide on claims filed before its office. It is only after the lapse of the given period can the taxpayer invoke the judicial remedy and appeal to the courts. Once the claim is elevated to the tax court, the BIR loses its authority to process the claim. This effectively addressed the issues raised under the old rules on the timing of judicial appeal and on the overlapping exercise of authority by the BIR and the courts.

There were also other issues under the old rules which I have been wanting to be resolved with the enactment of the EOPT. These concern the mandatory documentary requirements in administrative claims for refund. To recall, in the past, some applications were being denied for failure to present the originals or the certified true copies of the withholding tax certificates, and the proofs of remittance of taxes withheld. As the 180-day period commences to run from the date of submission of complete documents, I was also hoping for the BIR to settle once and for all the documents needed to be submitted upon filing the applications for refund – a call which the BIR heeded recently.

Early in July, the BIR issued RMC No. 75-2024, prescribing the mandatory requirements in claiming for refund of excess and unutilized CWTs, and RMO No. 25-2024, providing the guidelines, policies, and procedures in processing CWT refund claims.

Under RMC No. 75-2024, the application must be accompanied by the following documents: (a) Application for Tax Credit/Refund (BIR Form No. 1914); (b) Audited Financial Statements (“AFS”), complete with Notes to AFS, if the AFS was not submitted in BIR eAFS; (c) original copies of the Certificates of Creditable Tax Withheld at Source (BIR Form No. 2307) or Withholding Tax Remittance Return for Onerous Transfer of Real Property Other Than Capital Asset (BIR Form No. 1606), whichever is applicable, issued by the payor-withholding agent to the taxpayer-claimant; (d) hard and soft copies of Summary of Revenues/Income declared per Income Tax Return and the corresponding taxes withheld per BIR Form No. 2307/1606 in accordance with the BIR-prescribed format; (e) original duly notarized copy of Taxpayer’s Attestation, certifying to the taxpayer’s entitlement to the claim for refund, completeness and authenticity of the documents submitted, and availability of the taxpayer’s books of accounts and accounting records for verification; (f) proof of authority of the authorized representative of the taxpayer-claimant; and (g) original copy of Delinquency Verification Certificate which must be valid for six months. Only claims for refund filed with the documents mentioned will be accepted by the BIR.

This cleared all prior issues on refund. On the withholding tax certificates, the original copies must be submitted. Also, proofs of remittances of the withholding taxes are not required to be presented upon filing.

One particular provision in the RMO nonetheless concerns me. While the taxpayer-claimant is not mandated to submit proofs of remittance of the CWTs, the BIR may still verify whether the taxes withheld on income were remitted to the government. So, this leaves me to think on the effect of the results of that verification on the refund claims of the taxpayers. I hope that this will not adversely affect their claims.

To reiterate, one of the long-established conditions in claiming for refunds of excess and unutilized CWTs is the proof of withholding. But the proof of actual remittance by the withholding agents of the taxes withheld is not needed. The remittance of the taxes is the responsibility of the withholding tax agent, and not of the taxpayer-refund claimant. The latter precisely has no control over the remittance of the taxes withheld on its income. Hence, the taxpayer whose income has been subjected to withholding taxes should not be prejudiced by the act of the withholding agent. The withholding tax certificates will serve as proofs of actual payment of the withholding taxes to the government (G.R. No. 180290, September 29, 2014).

----------------------------------------------

For inquiries on the article, you may call or email

ATTY. MABEL L. BUTED

Junior Partner

T: +63 2 8403 2001 loc. 160

This email address is being protected from spambots. You need JavaScript enabled to view it.

DISCLAIMER: The contents of this Insights are summaries of selected issuances from various government agencies, Court decisions and articles written by our experts. They are intended for guidance only and as such should not be regarded as a substitute for professional advice.

Copyright © 2024 by Du-Baladad and Associates (BDB Law). All rights reserved. No part of this issue covered by this copyright may be produced and/or used in any form or by any means – graphic, electronic and mechanical without the written permission of the publisher.